Can a Bank Be Held Liable to Compensate for Unexpected Theft From a Locker? Amount of Compensation

Can a Bank Be Held Liable to Compensate for Unexpected Theft? Know about the latest trends in the Law surrounding the Liability of Banks in case of an Unexpected Theft, Amount of Compensation, with Decided Judgments

Author, THelawcritiQue

11/11/20257 min read

Can a Bank Be Held Liable to Compensate for Unexpected Theft From a Locker? Amount of Compensation

Introduction: The Myth of Absolute Safety

It is a general perception that when you deposit or store something in a bank locker, it is believed that the Bank is absolutely liable for our things in any case. For many people, a bank locker represents absolute safety in any case what so ever. We deposit jewellery, property documents, heirlooms, or savings bonds in those tiny steel boxes, believing they the Banks will save them from any possibility of thieves or natural calamities. But consider if a Bank locker is broken by thieves or if the contents of the locker vanished due to natural calamity such as sudden fall of building or earthquakes. Can the Bank be held liable for the lost contents of the locker?

The truth is actually disappointing to many trusting customers. While Banks are responsible to provide with reasonable security and a duty of care to their customers, at the same time they are not absolute insurers of locker contents. The liability of banks in cases of theft or loss depends locked items depends on the degree of negligence, contractual terms, and guidelines issued by the Reserve Bank of India (RBI) following landmark judicial pronouncements.

This article explores about the complex analysis of liability of Banks with reference to Judicial pronouncements and Reserve Bank of India Guidelines to give a proper outline of how much a Bank can be made liable and under what circumstances.

Renting a Bank Locker is a Contract of of Bailment, Not Insurance

Every customer who rents a Bank Locker is in a contract of Bailment with the Bank as defined in the Indian Contract Act, 1872. That means the relationship between the customer and the banker is that of a bailor and bailee but it is not that of insurer and insured. Section 148 of Indian Contract Act, 1872 defines bailment as the delivery of goods from one person (the bailor) to another (the bailee) for a specific purpose, with the condition that the goods shall be returned once the purpose is accomplished. While the bailee has responsibility to take reasonable care of the goods deposited, he is not absolutely liable for any loss occurred without his negligence. Thus, a banker is also liable to keep safe custody of the goods deposited only but not liable to the losses occurred due to external factors. In the case of a contract of insurance there is no such limitation of negligence. The insurer is liable to cover the loss occurred even due to the negligence or mistake of any third person or external factor.

In the context of bank lockers:

The customer is the bailor, who entrusts his valuable items to keep safe custody with the bank.

The bank her acts as the bailee, which shall be responsible to take reasonable care of the locker ensuring that it is secure against unauthorized access.

However, this liability does not make the bank an insurer of the contents in the locker. The Bank shall take care of the locker to the same level of a prudent man would look after his own property. Therefore, in case of a theft occurred, the question is whether the bank took reasonable precautions to secure the vault against the theft and if the answer is affirmative the bank need not be held liable for any of the contents of the locker.

The Turning Point: Supreme Court’s 2021 Judgment

The discussion about the liability of the bank regarding the contents of the locker came before the Supreme Court of Indian in the landmark case of Amitabha Dasgupta v. United Bank of India (2021 SCC OnLine SC 124).

The facts of the case are as follows - Mr. Dasgupta had rented a locker with the United Bank of India. One day, he found that the bank had broken open his locker without informing him, citing non-payment of rent. After checking he claimed that several of his valuables were missing. Consequently the bank denied liability regarding any of the contents as claimed stating that it had no knowledge of what was kept inside the locker and claimed it could not be held responsible for the loss.

The Supreme Court’s Ruling - The Supreme Court rejected the bank’s vague claim of no responsibility as to the security of the locker saying that: ----

A bank cannot deny its liability of maintaining the safety of lockers from any external threats and ensuring their proper operation.

Bank not having knowledge regarding due to customer’s non disclosure of locker contents does not absolve the bank of liability in case of negligence or deficiency in service.

Banks have a fiduciary duty to protect lockers and must maintain a transparent and accountable system.

The Court observed:

“It is not possible for the banks to contract out of their responsibility towards customers regarding maintenance and security of the locker systems. They are under duty to exercise due diligence in providing safety and security of the lockers.”

In this case, the Court awarded a compensation of ₹5 lakh to the petitioner underlying the negligence of bank in maintaining the safety. The Court also directed the RBI to establish comprehensive guidelines in this regard to ensure better protection of locker facilities and curtailing the banks' escape routes in case of its negligence by claiming it do not know what are the contents of the locker.

Thus, a bank is not automatically liable to indemnify the loss of the customer, but where negligence, mismanagement, or deficiency in service is proven, the bank must compensate the customer.

RBI’s 2021 Revised Locker Guidelines

In consequence of the direction of the Supreme Court in Amitabha Dasgupta's case the Reserve Bank of India issued Revised Guidelines on Safe Deposit Lockers on 18 August 2021, which came into effect from 1 January 2022. These guidelines outline the extent of bank's liability and strengthen customer rights.

The Key Provisions of the Guidelines include

Obligation of Due Diligence to Maintain Security

Banks must provide a robust locker management system, with adequate CCTV coverage, electronic records of locker operations.

Ensure the integrity of the locker keys to the customer himself and in any case prevent unauthorized access not just to outsiders but even to its employees.

Extent of Liability in Case of Unforeseen Events such as Theft, Fire, or Natural Disaster

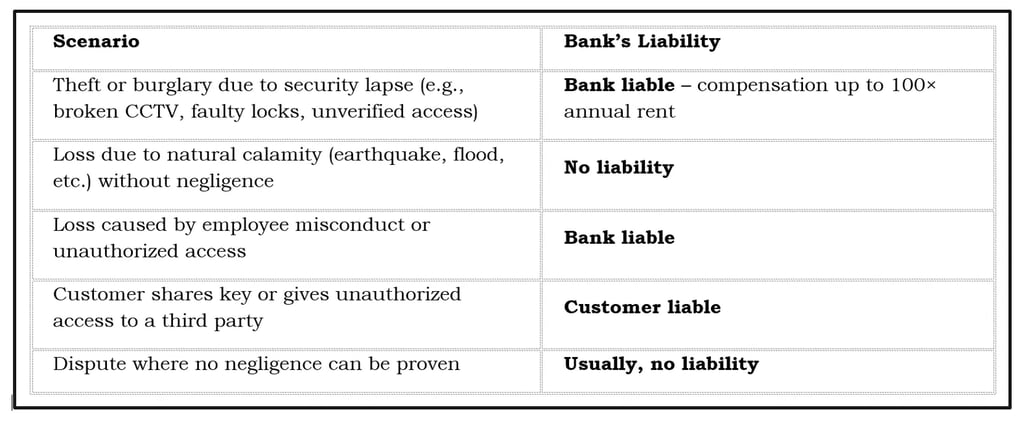

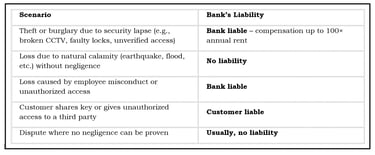

The fact that is to be seen is whether there is any negligence or deficiency in service on the part of the bank. If it is proved that the customer's items are lost due to negligence of the bank, the bank’s liability is capped at 100 times the annual rent of the locker.

For example, if the locker rent is ₹3,000 per year, the bank’s maximum liability would be ₹3,00,000. Whereas no liability can be invoked against the bank if there is no negligence or deficiency in service of the bank.

Disclosure and Accountability as to the Terms

Banks must give the copy of locker agreement to the customer which clearly outlines their responsibilities and their position as a party to contract. The liabilities and the rights of customers shall be disclosed at the time of the agreement itself.

Customers must be informed that the bank is not aware of the contents and does not provide insurance of the terms automatically.

Third-Party Insurance Option

While banks themselves does not act as insurers of the are not insurers of the contents, they may offer insurance facilities to the customers, through third parties is the customer wishes to cover the items in their locker.

When Is the Bank Liable?

A bank’s liability is determined primarily by checking if there was any negligence or deficiency in service in maintaining its lockers. Thus, banks are not automatically not liable but only becomes liable when they are found guilty of negligent conduct, mismanagement or violation of RBI’s locker guidelines. Courts and consumer forums will examine whether the bank took necessary precautions to ensure the safety of the locker.

Our Critique - What Should Locker Holders Do?

Though the new guidelines gave customers stronger protection, still the same is not absolute. Even if the bank is found negligent, its liability cannot exceed over 100 times the locker's annual rent, which in most cases is far lesser than the valuables of the customer. Therefore, locker holders must also take proactive steps to safeguard their interests:

Maintain a Due Record of Inventory and Valuation of items kept in the locker. Take photographs, get bills or valuation certificates that can properly access and audit the value of your items so that it can help to substantiate claims in the event of any loss due to management issues.

Do not allow access or locker key of your locker to anyone else other the persons authorized in the agreement. This gives undue advantage to the bank to deny its not responsible even in the case of loss occurred due to its negligence.

Insure your valuables separately - These days may third party companies provides insurance to valuables such as jewellery, electronics, house or documents. Insuring valuable items against possible unforeseen events is always a good safety step in advance.

Report any malfunction or tampering - In case of locker key malfunction or inadequate to provide safety to the valuables immediately report the same to bank in writing and ask for a replacement.

Renew the locker rent on time and keep acknowledgments of all payments to ensure due deligence and also verify the records of the locker frequently.

The decision of the Supreme Court in 2021 marked a clear shift of perspective from 'purely contractual liability to return goods' to that of the one that recognizes the 'fiduciary duty the banks owe to their customers' to protect and secure the lockers with prudent care. The RBI’s guidelines further strengthened this shift by defining standards of care banks owe and by setting the amount of compensation in event of found negligence.

However, the 100 times annual rent compensation limit has attracted mixed views. While some argue to provide absolute security or at least a proportionate of value of the locker, some advocate that the banks shall not be held responsible for what they cannot control. In most high-value cases, the compensation amount may be inadequate compared to the actual loss of items occurred. Legal experts suggest that customers should still pursue to claim higher compensation through consumer complaints or civil suits by proving the actual value of lost goods and negligence on part of the banks.

Conclusion: Shared Responsibility, Defined Boundaries

In conclusion, a bank locker is secure but not infallible. The law today strikes a balance between protecting the customer and not over-burdening banks with unlimited liability at the same time. From the passive view of 'we don't know what you deposited so we are not liable' the courts took a passive approach to establish - 'you cannot evade complete responsibility' but not overburdening them with good to good replacement and limiting their role only to a compensation for negligence.

The relationship shall be the kind of trust with accountability - banks must ensure robust systems and transparency, while customers must act prudently and maintain evidence of their valuables. No bank can evade responsibility under the guise of ignorance or technicalities.

Also read our article on - Live-in relationships in India, Legality and Social Stigma

Connect With Us Through

Connect with us

© 2025. All rights reserved.