Consequnces of Signing a Blank Cheque | Legal Risks and Presumptions Explained

Discover the legal consequences of signing a blank cheque in India. Learn about criminal liability, Section 138 NI Act, and key legal defences to protect yourself.

Author, ThelawcritiQue

10/30/20258 min read

Consequences of Signing a Blank Cheque.. Ingredients attracting Criminal Liability

Introduction: The Real Consequence of a Simple Signature

We usually come across with a necessity to sign a blank cheque in various places. Whether it be a friend, colleague, or business associate or even banks when they offer loan, may ask you to sign a blank cheque — as security for a loan, rent, or business deal casually to use it “just in case”. You sign and deliver trust initially maybe out of trust or due to dire necessity. When you almost forgot about it, months later you receive a legal notice under Section 138 of the Negotiable Instruments Act, 1881, accusing you of issuing a cheque that bounced due to lack of funds.

Well this isn't an unfamiliar situation to any one. In a country like India thousands of people everyday encounter criminal proceedings just because they sign a blank cheque without knowing the criminal consequences the dishonour of a cheque carries.

In this article we break down about what really happens when you sign a blank cheque, what legal presumptions can be invoked against you in the case of signing a blank cheque, legal remedies that can be utilized in such cases along with case law analysis.

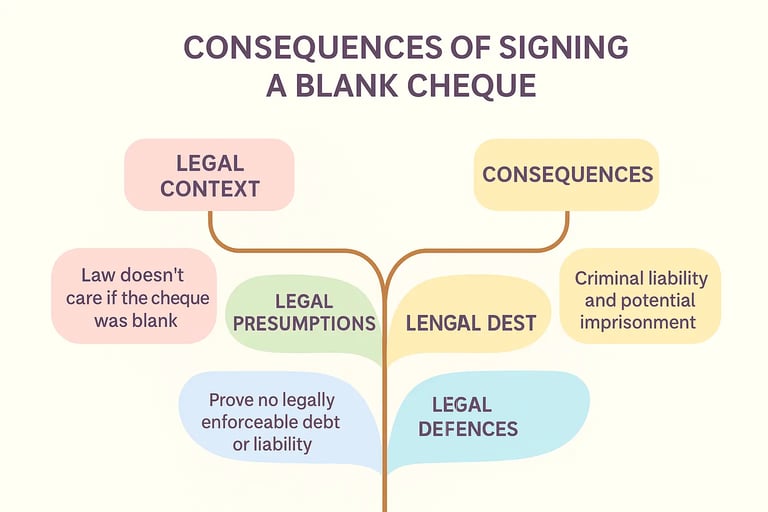

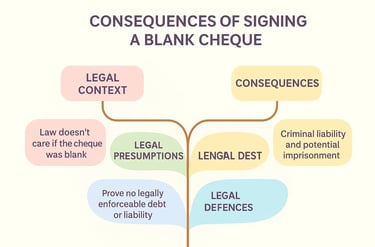

Legal Context: Law Doesn’t Care if it was a Blank Cheque or a Filled Cheque.

Section 138 of the Negotiable Instruments Act (NI Act) - The Section clearly states that if a cheque is dishonoured 'due to insufficient funds', the drawer i.e., the person who issued the cheque shall be deemed to have committed an offense punishable — up to two years imprisonment or fine up to twice the cheque amount.

... discharge, in whole or in part, of any debt or other liability. — it is also required that the cheque must be issued by the drawer for discharge, wholly or in part of a debt or a liability. But this is where Sec. 139 comes into action. It says that unless the contrary is proved it shall be presumed that the drawer has issued the cheque for discharge wholly or in part of a debt. That means the duty to prove there is no legally enforceable debt is on the drawer but not the holder.

But here’s where people go wrong:

Common misconception is the people still think proving the cheque was blank at the time of issuance can cover the presumption. In fact it is contrary. Even if you claim that the cheque was signed blank and misused later, the law presumes it was issued for a legally enforceable debt and Section 139 of the NI Act still operates.

This presumption is automatic and against the favour of the drawer. It means the burden is on drawer to prove otherwise. The Supreme Court in Bir Singh vs . Mukesh Kumar, (2019) observed the accused admitting the issuance of cheque in a blank condition but held him liable - “A cheque duly signed by the drawer, even if voluntarily handed over blank, attracts presumption under Section 139. The burden to rebut lies upon the accused.”

In simpler terms — once your signature is there on a cheque and the cheque gets bounced, you’re presumed to owe the money, unless you can prove contrary.

Understanding the Legal Presumption under Section 139

Section 139 reads as follows :

“It shall be presumed, unless the contrary is proved, that the holder of a cheque received the cheque... for the discharge, in whole or in part, of any debt or other liability.”

The presumption implies that — once complainant presents a cheque signed by the accused the court has to assume that

The accused issued it voluntarily, and

It was meant to repay a debt or liability.

The plea by the accused that - “He didn’t fill the amount” or “It was taken as a security for a liability but not to en-cash” will not automatically work unless with credible evidence to convince the court otherwise.

What Happens When a Blank Cheque Is Misused?

The possible consequences of a person fills out and deposits a blank cheque issued by a drawer without his consent, and it bounces, the account holder will receive:

A demand legal notice within 30 days of dishonour, will be sent to the accused - demanding payment within 15 days of receiving the same -- as required under (a) to proviso under Section 138 of NI Act; and

On failure to make payment within 15 days as demanded - Possible criminal complaint under Section 138 r/w 142 of Negotiable Instruments Act.

Once the case is filed, the court process begins — summons, trial, and if the merits in favour of the complainant a potential conviction shall follow. Even if the accused is innocent, he still need to defend his case by hiring a lawyer and produce evidence showing misuse.

Precautions that can Prevent the Misuse of a Cheque issued in Trust - Legal Defences That can be Invoked ..

In a criminal prosecution of a cheque dishonor case the following legal defences can be resorted to effectively defend your case and avoid punishment.

1. Proving of "No Legally Enforceable Debt or Liability" Existed is of Paramount Importance

In any case of misuse of a cheque or dishonour of cheque cased, showing that you didn’t owe any money to the complainant when the cheque was given can completely vitiate the trail and tear down the prosecution. The accused can establish no liability or debt by relying on any evidences such as -

Written communication by the complainant - Even through WhatsApp, email, SMS showing it was only taken as a “security” but there is no liability or debt may help.

The accused can also rely on lack of financial transaction records proving any loan or consideration passed to the accused from the complainant.

Statements of any direct witnesses that support the version of the accused.

2. Reporting to Police about missing cheque

If there is a strong reason that the cheque was misused or stolen, the accused can immediately file an FIR or non-cognizable complaint under Sections 420, 406 IPC for cheating and criminal breach of trust. This though requires the accused to prove, but it can strengthen the defense.

3. Issue an instruction to Bank to Stop-Payment

While the cheque was presented for collection, by that time itself you are too late. This cannot absolve you from liability that may be incurred, it certainly helps in establishing good defense, timely action and good faith. So whenever there is a misuse of a cheque issued by you it is always suggestible to instruct the banker to stop the payment of the cheque.

4. Ask for a Deed in Written

If the holder of a cheque can keep the custody of your cheque out of pure trust, it is never wrong to ask for a deed or agreement in written of why and when the cheque was issued, and for what purpose. Keeping a written record of the purpose and time of issuance of cheque, can give the accused a good defence. Never issue blank cheques without a written understanding.

5. Issue a Reply to the Legal Notice within Prompt Time

No offence can be made out under section 138 of Negotiable Instruments Act without sending a legal notice to you demanding to pay the due amount within 15 days. Therefore, 15 days is the statutory time the accused. So when the accused receives a notice under Section 138, promptly reply within 15 days, by clearly mentioning the defence that he is going to take at the time of trail. Ignoring the notice can lead to fatal consequences to the case.

Key Judicial Precedents

ICDS Ltd. v. Beena Shabeer (2002) – The Supreme Court held that - even a cheque issued as security to a loan or debt can attract liability under Section 138 if it is in the due course of a legally enforceable debt or liability on the date of presentation.

Bir Singh v. Mukesh Kumar (2019) – Held if a cheque was signed voluntarily and handed over to the complainant, it is valid to draw presumption under Section 139; and it is the duty of the accused to rebut it with evidence.

Rangappa v. Sri Mohan (2010) AIR 2010 SUPREME COURT 1898 – When the accused fails to prove the issuance of blank cheque, not issuing of reply to legal notice, no sufficient grounds to believe the version of the accused, the presumption under Section 139 cannot be rebutted. The presumption includes both the existence of debt and the intention to discharge it.

Preventive Tips to avoid being Trapped in Criminal Litigation

Never sign blank cheques.- In unavoidable cases of necessity, cross it (“A/C Payee Only”) and mention “for security only” in writing and also get a written understanding as to why the cheque was given and for what purpose it has to be used.

Keep limited cheque leaves active.- Destroy unused cheques responsibly.

Use written agreements.- Ask the holder to write an agreement regarding the purpose of issuance of cheque, debt or security.

For every payment made to the holder or the complainant Prefer digital payment or if it is not possible or if the holder did not allow the same, get a written receipt from him to prove payments.

Our CritiQue: On How Trust leads to Criminalisation

Section 138 of the Negotiable Instruments Act was designed to curb the cases of cheque dishonour by penalizing the act done due to willful default by the persons who uses it as a tactic. It was not intended not to punish naive or trusting individuals who sign blank cheques in good faith to give them as a security or get of a necessity. The law intends to to promote honesty and value the promise given in financial transactions — but in practice, it criminalises trust activities done in good faith.

The presumption under Section 139 is powerful and essential in cases of breach of trust and misappropriation of money, but it in most number of cases it often shifts the balance unfairly against the accused. The signature of a person becomes an instrument of self-incrimination, even without consideration formed out of pure trust.

Moreover, there is a rampant misuse of post-dated or security cheques that has turned Section 138 cases into a litigation weapon to force the innocent trusted accused to attain for a settlement with the accused. Present day courts are flooded with such cases of vindictive litigation stemming not from fraud, but from misplaced trust. In these high circumstances changing day by day, a reform is overdue. India needs a system that can establish a clear distinction between security cheques and payment cheques to avoid the harassment to the innocent ones to issues the cheque out of pure trust or security or dire necessity. Until then, the safest legal advice remains simple:

"Never sign a blank cheque — not even for family."

Frequently Asked Questions (FAQs)

1. Can I go to jail for a blank cheque that bounced?

Yes. If the cheque bounces and you fail to prove it was misused, Section 138 can lead to imprisonment up to 2 years or fine up to twice the cheque amount.

2. Can I prove that the cheque was only for security?

Yes, but the burden lies on you. You’ll need evidence such as written communication, lack of financial transaction, or witness statements.

3. Can a stop payment prevent liability?

No, stop payment does not automatically protect you. The court will still presume liability unless you rebut it with evidence.

4. Can the complainant fill in any amount they want?

Technically, if you signed and handed over a blank cheque, they can fill in the details — but doing so without your consent is criminal misuse, which you must prove.

5. What’s the safest alternative to giving a blank cheque?

Written security agreements, post-dated signed cheques with amount and date filled, or digital transfer proofs.

Final Word from ThelawcritiQue

A cheque is not just a piece of paper that can be given as a security it is an instrument — it’s a promise backed by law. When we sign it blank, we surrender to the for unforeseen or unintentional control over that promise. In a legal system that outweighs presumption over intention, our own signature can mark to be our penalizing mistake.

So, before signing a blank cheque — remember, in law, trust without evidence is just a risk with ink.

Read more on : Evidence of Sexual Intercourse in Rape Cases

Connect With Us Through

Connect with us

© 2025. All rights reserved.